-

Chinese investors dominate the market, and focus on yields

-

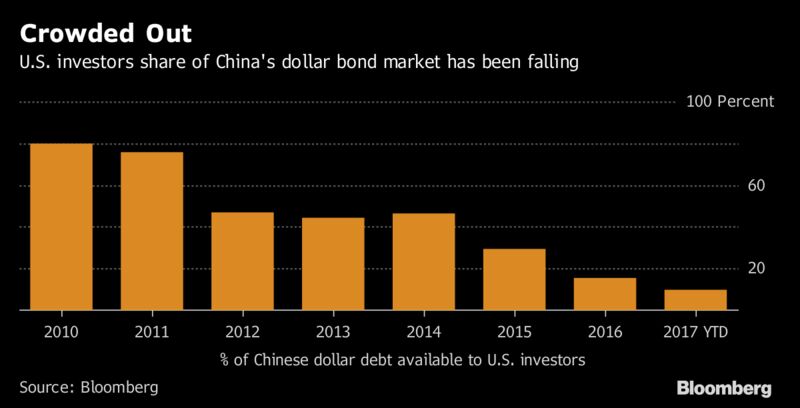

Issuers from the nation sell less offshore than neighbor Japan

The S&P Global Ratings downgrade, which came more than four months after Moody’s Investors Service did the same, has barely registered in China’s bond markets. Case in point: state-run lender Postal Savings Bank of China Co. sold the most dollar debt since Alibaba Group Holding Ltd. in 2014, just a few hours after the S&P announcement.

While credit-rating changes in any case have a varied track record when it comes to influencing pricing over the longer term, China’s debt landscape is much more insulated than for other developed and even emerging nations, given the Communist Party’s top-down control of the economy and financial markets.

These are the main reasons why this rating cut is a non-event for bonds:

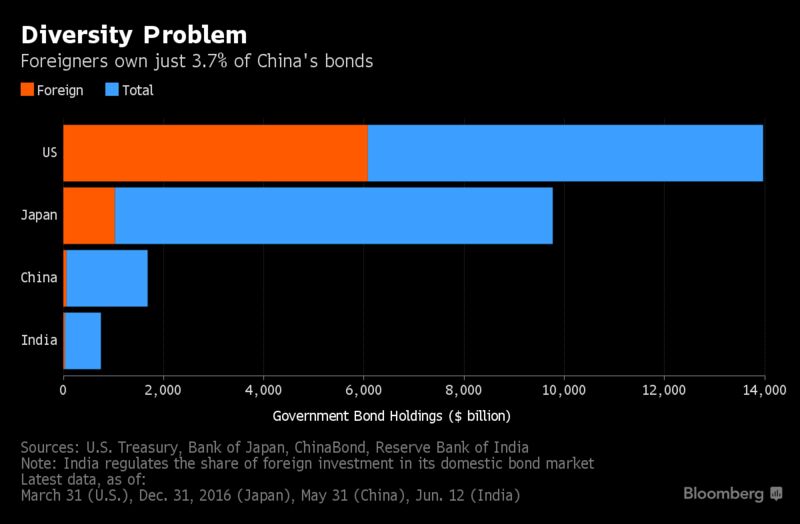

1. Chinese own most of the debt

Hurdles for investment from outside mean foreigners make up only a minuscule portion of China’s onshore bond market, even as Beijing tries to redress that through initiatives like the connect with Hong Kong, set up in July. Chinese investors are less likely to place importance on the views of western ratings agencies, especially when you have officials and the state media trashing their assessments.China’s Finance Ministry said S&P had made the “wrong decision,” ignoring the country’s sound economic fundamentals and ability to bail itself out.

Company sales of dollar-denominated bonds have risen to a record $133 billion this year, and the first sovereign sale since 2004 is in the offing.

2. Yields are really high

For Chinese investors it’s all about the yield, with domestic buyers tending to overlook red flags that may give investors outside of China pause because of the perception Beijing will bail out delinquent issuers.While that view is shifting as the authorities allow more defaults, China’s credits offer a significant premium for exposure to the world’s second-largest economy and consumer market.

3. The State

China wields a lot of control in its home markets, and while its activities may not always have the desired consequence -- as 2015’s boom-to-bust stock rout exemplified -- officials are apt to smooth asset swings, especially ahead of key political events.While there’s little suggestion the authorities are intervening following S&P’s move, the hand of the state was suspected after Moody’s cut as Chinese stock losses disappeared in a single trading session and the yuan soared despite depreciation pressures at the time.

China has also been using capital controls this year to ease speculative pressure on the yuan.

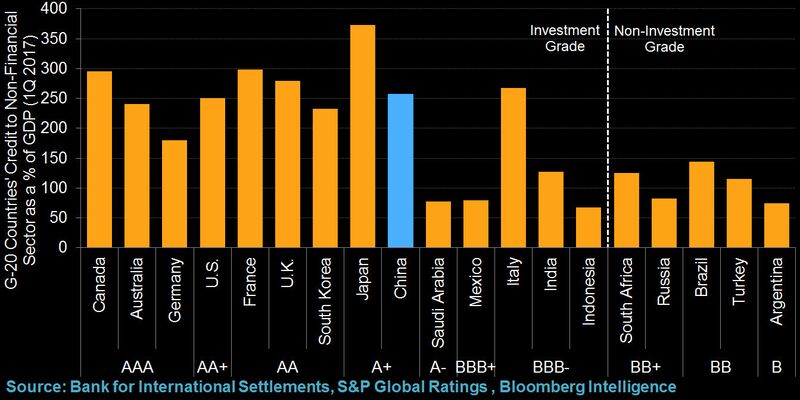

4. Corporate debt isn’t that bad

While the jury is still out on Chinese bank leverage, debt-to-equity ratios for companies have actually been falling, with levels for the largest non-financial firms the lowest since 2010.S&P cited a return to corporate credit growth of about 10 percent in its reasoning for the sovereign-rating cut. But Allianz Global Investors sees improvement, with debt expansion slowing from a peak of as fast as 14 percent in 2016 to under 9 percent in August, according to Morgan Lau, a portfolio manager for fixed income in Hong Kong.

So S&P may be late to the party on this one.

5. China has very little foreign debt

China doesn’t borrow much abroad, which also limits the impact of ratings downgrades.

— With assistance by Emma O'Brien, Finbarr Flynn, Narae Kim, Eric Lam, Denise Wee, Lianting Tu, David Yong, Tom Orlik, and Justin Jimenez

SOURCE FOR THIS ANALYSIS IS;BLOOMBERGY.COM

0 comments:

Post a Comment